A farmer outside Invercargill stands at a fence line and tries to picture it: the paddock across the road, not as grass and silage, but as Datagrid New Zealand, 78,000 square metres of humming hardware, swallowing more electricity than most cities and selling “AI factory” time to customers he’ll never meet.

He’s been told it will bring jobs, put Southland “on the digital map”, anchor young people to the region. He’s also read that the first 140MW of power, roughly 3% of the country’s total electricity, is already spoken for, locked into a 15‑year deal between Datagrid and Mercury.

The crucial thing about Datagrid New Zealand is this: it isn’t really a story about local jobs or even about data. It’s a story about who gets guaranteed access to New Zealand’s clean power for the next two decades, and who gets whatever’s left.

TL;DR

- Datagrid New Zealand is primarily a long‑term power allocation to offshore AI compute, not a sustainable regional jobs engine.

- A 15‑year, 140MW deal gives a private “AI factory” price certainty and continuous supply that ordinary households and local firms don’t enjoy.

- New Zealand is trading scarce, flexible renewable capacity for transient construction work, a few dozen permanent roles, and highly uncertain tax and ownership upside.

What is Datagrid New Zealand?

On paper, Datagrid New Zealand is a NZ$3.5 billion hyperscale data centre campus on farmland at Makarewa, near Invercargill. Phase one is 140MW; fully built, it’s 280MW, enough to handle about 70% of Christchurch’s current electricity demand.

The founders are familiar telecom names: Rémi Galasso of the Hawaiki submarine cable, and CallPlus co‑founder Malcolm Dick. Their pitch: build New Zealand’s first dedicated “AI factory”, strap it to a new 6,000km Tasman subsea cable to Sydney and Melbourne, and sell compute cycles to global AI clients.

By 2028, if everything lines up, funding, cable, grid connection, that paddock is meant to be an industrial node in the global AI supply chain.

Here’s where the story gets strange: once you subtract the marketing, what Datagrid mostly does is turn Southland water and wind into GPU time for other people’s models.

Why this is a power‑allocation story, not a jobs story

The official numbers are smooth and familiar: 1,200 construction jobs, “spillover benefits”, “high‑value roles”. The kind of phrasing you can hear in any regional ribbon‑cutting.

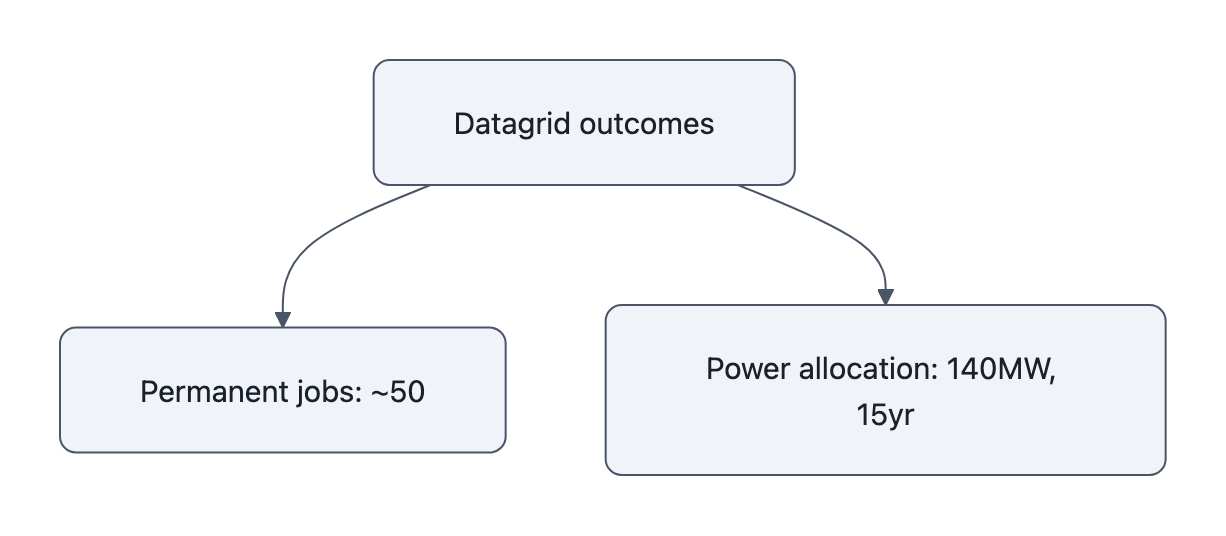

But the long‑term operational headcount is closer to 40-50 highly specialised staff, many likely flown in or recruited from a thin local talent pool. Hyperscale data centres are intentionally boring on the employment front: that’s the point of hyperscale. Automation, remote management, lights‑out operation.

Datagrid’s own power numbers, by contrast, are not boring at all.

- 280MW of capacity approved.

- 140MW already optioned from Mercury in a 15‑year power purchase agreement, around 1.2 TWh a year.

- That 140MW alone is about 3% of New Zealand’s entire annual electricity demand.

Those numbers tell you what Datagrid really is: a decision to earmark a chunk of the country’s clean, firm-ish generation for one industrial user whose product, AI compute, is overwhelmingly for export.

You can move engineers and GPUs. You cannot move Lake Manapōuri.

So when the project is sold as “3,000 jobs over the life of the build” and “a handful of high‑skill positions”, the scale is inverted. The permanent thing is not the payroll. It’s the power deal.

Who actually benefits from the ‘AI factory’?

Follow the electrons and follow the money; they do not end up in the same place.

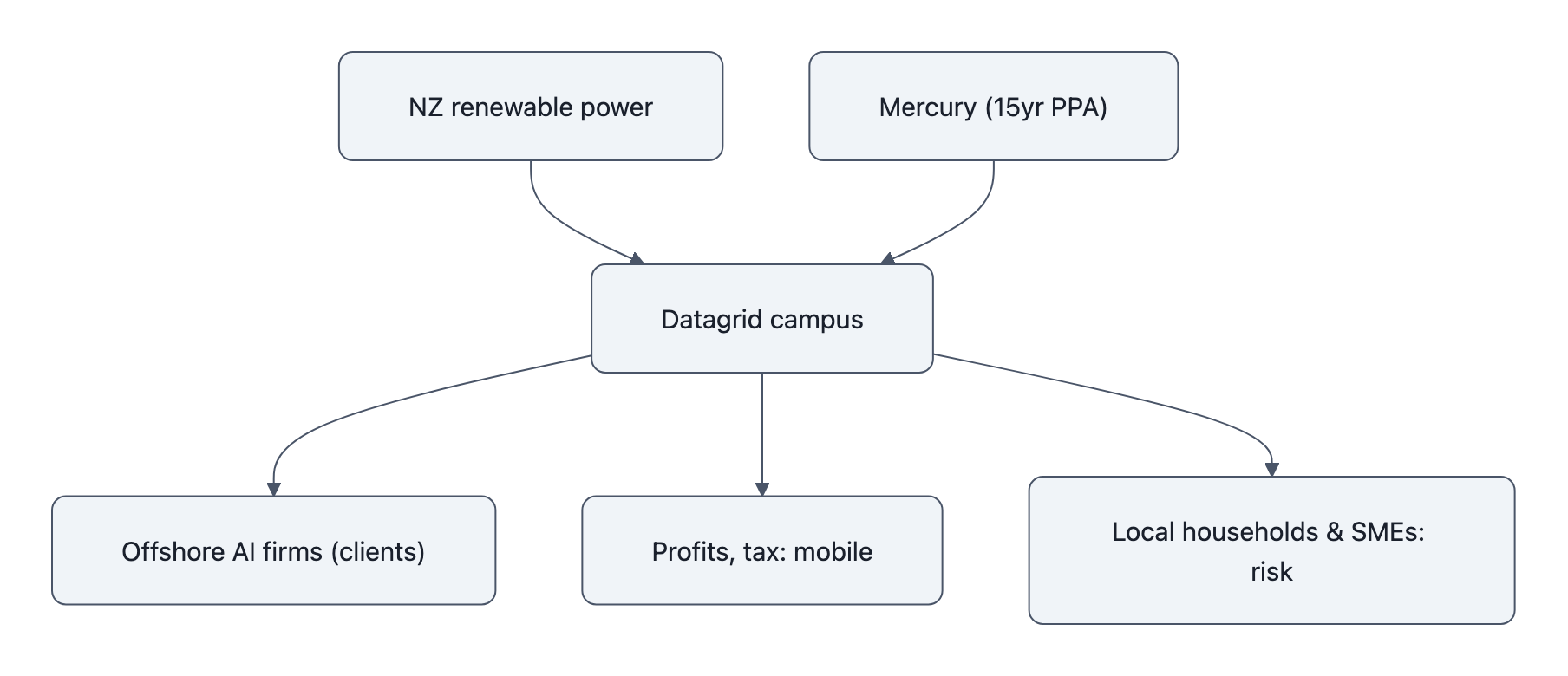

On the power side, Datagrid New Zealand enjoys:

- A 15‑year fixed‑price hedge from Mercury, majority‑owned by the government.

- Priority, continuous load. Unlike the Tiwai Point aluminium smelter, you can’t just “turn down” AI racks in a dry year without risking equipment and contracts.

On the revenue side, the campus will mostly be serving international AI customers via the Tasman cable, co‑located training runs, inference workloads, “AI factories” in the Nvidia sense of the term. The profits from that work are very likely to live in the usual places: parent entities in Australia, Singapore, the US.

New Zealand has already seen this movie. Local subsidiaries of Google, Meta, Amazon Web Services report hundreds of millions in revenue but pay low single‑digit millions in corporate tax, thanks to service fees and intellectual property charges wired offshore.

An AWS example from RNZ: NZ$385m in local revenue, NZ$1.7m in tax.

Nothing about Datagrid’s structure guarantees it won’t follow the same pattern: the physical plant anchored here, the high‑margin value captured somewhere else. The power is local and long‑term; the profit can be mobile and optimised.

Meanwhile, who absorbs the risk?

- Households and small businesses still face spot‑price volatility and dry‑year spikes.

- Other electricity‑intensive industries, including any future domestic AI startups that need serious compute, will compete with a locked‑in 140-280MW draw that can’t flex down in a crunch.

- Taxpayers, as majority owners of Mercury, underwrite a generator that has chosen to reserve a large slab of future output for a single customer.

New Zealand is not alone here. Globally, we’ve been very quick to count “AI jobs” and very slow to ask who benefits when AI consumes infrastructure. Our own piece on AI and unemployment made this point at the labour level. Datagrid forces the same question at the level of rivers and pylons.

The unresolved hurdles that make consent conditional

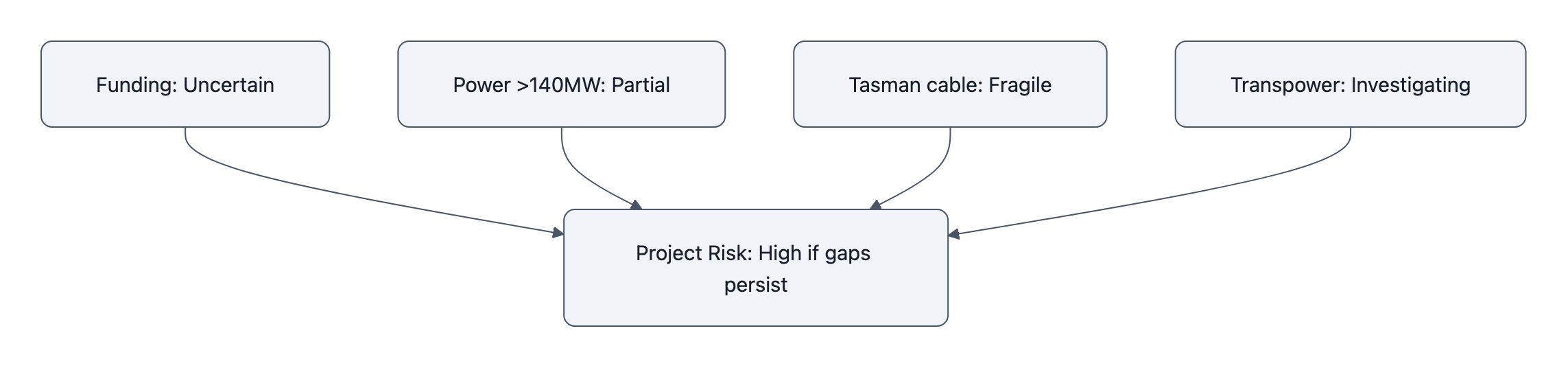

All of this assumes Datagrid New Zealand actually gets built as advertised. That is not a trivial assumption.

Several key parts of the puzzle remain blurry:

- Funding: billions in capex are still not publicly lined up. Hyperscale builds are capital‑intensive, cyclical, and extremely sensitive to interest rates and GPU supply.

- Power beyond 140MW: only half the eventual 280MW is tied down. Meridian, once an active partner, now describes itself as merely “interested”. Contact and Genesis are noncommittal.

- Subsea cable fragility: Chorus has pulled out of the Tasman Ring Network partnership, even as government briefings describe the cable as “essential” for Datagrid’s business model.

- Transpower connection: the grid connection process is still at an “investigative” stage, typically a multi‑year, non‑guaranteed endeavour.

In other words: the country has already agreed to rezone the paddock and plan for a 280MW load. But the corporate structure stitching that load into the global AI economy is still being negotiated, refinanced, and re‑partnered.

This asymmetry matters. Once you’ve built extra transmission capacity and normalised the idea that Southland’s spare renewable capacity is an export commodity, something will fill it, Datagrid or its successor. It is much harder to walk back a grid reconfiguration than to walk away from a single data‑centre project finance deal.

What Datagrid reveals about NZ’s infrastructure priorities

If you zoom out a little, Datagrid New Zealand looks less like an outlier and more like a test case.

New Zealand keeps talking about data centres as if they are software parks or call centres: regional development tools, fodder for employment statistics, proof we’re “part of the AI wave”. But infrastructure doesn’t care about press releases. It cares about what gets built, who gets to plug into it, and under what terms.

A few questions crystallise:

- If 3-6% of national electricity is going to an AI export factory, what projects do not get built or expanded over the next 15 years?

- Should an offshore‑facing data centre have stronger obligations around demand flexibility, especially in dry years?

- Are we comfortable giving one private operator more price certainty than any household, while its likely upstream clients are the same multinationals we struggle to tax fairly?

These are not “AI ethics” questions in the abstract. They’re as concrete as a transformer yard and as political as a power bill.

They also tie back to accountability. The Datagrid campus will be part of the same AI infrastructure that raises hard questions when models are used in lethal targeting or mass surveillance, the kind of questions we wrestled with in our piece on AI accountability. Once you’ve devoted 280MW of clean power to that global machine, it is harder to pretend you’re just a neutral host.

The farmer at the fence line is making his own, quieter calculation. He’s heard about the school lunch cuts, the hospital waitlists, the renewable projects stuck in planning. He knows this region has been trading resources for promises since aluminium and sheep.

If Datagrid New Zealand really is our first “AI factory”, then the first honest step is to stop calling it an employment scheme. It’s an energy treaty, signed on behalf of future power users who don’t yet know they’re at the table.

Key Takeaways

- Datagrid New Zealand’s core feature is a 15‑year, 140MW power deal, not thousands of permanent jobs.

- The project reallocates 3-6% of national electricity toward offshore AI compute, with minimal flexibility in dry years.

- Long‑term value is likely to accrue to offshore tech firms and holding companies, while New Zealand supplies land, water, and grid capacity.

- Significant hurdles, funding, full power contracts, subsea cable, grid connection, mean the infrastructure commitment may outlast this specific company.

- Treating Datagrid as a standard “regional investment” hides the real trade: guaranteed clean energy out, uncertain economic return back.

Further Reading

- Datagrid signs 140MW deal to power Southland AI campus, Coverage of the 15‑year power purchase option with Mercury and key project specs.

- New Zealand’s Datagrid gets approval for 280MW campus near Invercargill, Details of the resource consent and design of the hyperscale campus.

- A new Southland datacentre would be the country’s second-largest drain on power, RNZ analysis of Datagrid’s likely power draw and implications for the national grid.

- Democracy Briefing: The hard questions behind Southland’s AI factory, Critical examination of who benefits and why Datagrid is really a power‑allocation story.

- Fears new data centre could bump up power bills, Reporting on concerns around electricity pricing, dry‑year risks, and the Datagrid-Mercury power deal.

In a few years, if you drive past Makarewa at night and see a new glow on the horizon, it won’t be a factory in any 20th‑century sense. It will be thousands of machines turning Southland’s rivers into probability distributions, and the question will linger in the wind over the paddocks: whose future did we just power up?