On Citi’s trading floor, someone basically wrote: “AI might give us boom‑level productivity and still push us into a deflation scare.”

That’s the core of Citi’s AI deflation warning. Not “AI will kill growth.” The opposite: AI could boost output, but if almost all of that gain goes to a “small AI elite,” you can get strong growth coexisting with high unemployment and falling prices.

The interesting part isn’t the macro math. It’s the subtext: this is a political‑economy failure more than a technological one.

If you design institutions to funnel AI gains to the top, you don’t get a sci‑fi abundance utopia. You get a demand problem central banks can’t fix with rate cuts alone.

Let’s unpack that, and what levers actually matter.

What Citi Actually Said, and Why “AI Deflation” Is a Different Alarm

Citi’s public “Global Growth: More Resilient Than Ever” note (Feb 26, 2026) and a related client strategy note did something unusual for a big bank: they explicitly connected AI, inequality, unemployment, and deflation.

The strategists (led by Dirk Willer on the client note; Nathan Sheets on the research report) warned that:

- “Eventually AI implementation will lead to higher unemployment and deflation…”

- If productivity gains accrue to a “small AI elite,” growth can coexist with “unemployment and deflation.”

- In that world, the bias for US rates is “likely lower”, i.e., central banks would be stuck fighting disinflation with permanently easier policy.

That’s not another “robots will take all the jobs” op‑ed. It’s closer to:

“We can have more stuff, made cheaper, but not enough people with paychecks to buy it.”

The non‑obvious part of Citi’s AI deflation warning is this: the risk isn’t high productivity. It’s who gets the productivity.

If the gains show up as:

- 200% profit margins for a few AI platform firms, plus

- 10-30% wage cuts or layoffs for everyone else,

then the macro problem isn’t technology. It’s distribution.

This is the same basic theme we’ve written about in AI productivity and value capture: AI makes it easier to centralize value capture in whoever controls the rails.

Citi is just saying the quiet part out loud: if you centralize hard enough, the macro engine stalls.

How AI Deflation Actually Happens (The Economic Mechanism)

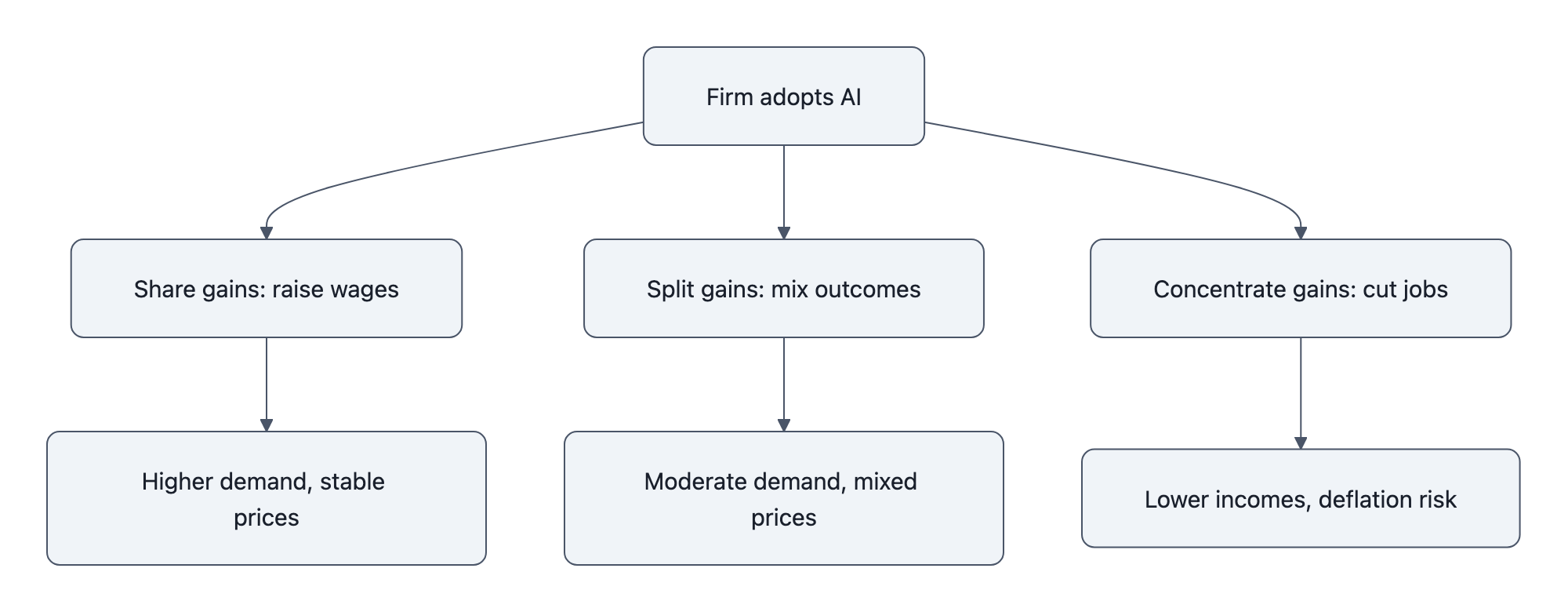

Forget DSGE models for a second. Picture a mid‑sized software company with 1,000 people.

They roll out an LLM agent stack that:

- lets every engineer ship 2-3x more features,

- automates 60% of L1+L2 support,

- and writes most of the internal reporting.

Management has three choices:

- Share the gains

Keep headcount stable, raise wages/bonuses, shorten hours, drop prices, reinvest in product. - Split the gains

Moderate layoffs, some wage pressure, some price cuts, some margin expansion. - Concentrate the gains

Fire 30-40% of staff, freeze wages, hold prices as high as competition allows, push margins to the ceiling.

The technology is the same in all three cases. The macro outcome is not.

Scale option 3 across thousands of firms and Citi’s AI deflation story appears:

- Supply goes up

AI lets the remaining workers produce more code, more content, more diagnostics, more everything. - Labor income goes down or stagnates

Automation replaces jobs, suppresses wages, and weakens bargaining power. - Demand lags

Households are most of final demand. Lower mass income means they can’t buy all that new output at current prices. - Prices get pushed down

Too much capacity + weak demand = firms cut prices to move volume (or try to, until market power gets in the way). - Central banks react

Persistent disinflation and unemployment → dovish bias, lower rates, maybe QE‑style support even with decent headline growth.

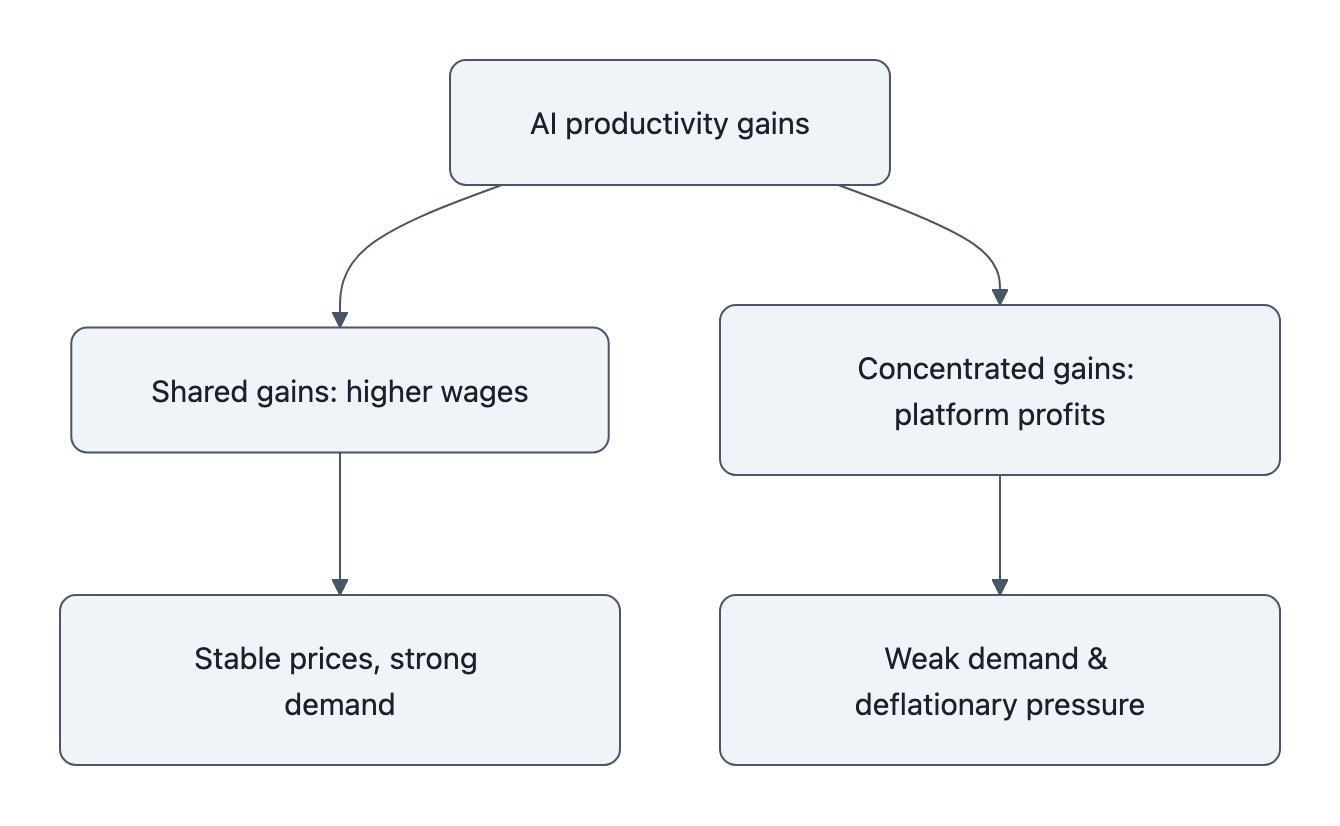

That’s AI-induced deflation in one paragraph: the machine makes more, the owners grab the proceeds, the customers can’t afford the surplus, and prices crack.

Notice what had to be true:

- AI is actually productive (this is the bullish part).

- Gains are heavily skewed (this is the political‑economy part).

- Product and labor markets are competitive enough that weak demand shows up as falling prices, not just shrinking variety or quality.

If you instead have concentrated AI power plus pricing power, you may get a weird mix: falling wages, sticky high prices, and terrible consumer surplus. That’s not classical deflation; it’s feudal SaaS.

But the engine driving both outcomes is the same: productivity concentration inequality.

How Plausible Is Citi’s Scenario? Timing, Evidence, and Caveats

Let’s be blunt: anyone telling you they know the exact timing of an AI deflation spiral is lying or selling something.

Citi doesn’t. Their own strategy note literally says the timing of large AI disruptions is “very unclear.”

The right question is: what’s the direction of pressure, and how fast can it build?

1. We’ve run parts of this movie before

Acemoglu & Restrepo’s “Robots and Jobs” paper (NBER) looked at US labor markets where industrial robots diffused. They found:

- Each extra robot per thousand workers reduced employment and depressed wages in affected commuting zones.

- The aggregate impact depended on how much new demand the cheaper, robot‑enabled output created.

Translation: automation can be both productive and labor‑displacing, and whether you get macro pain depends on downstream demand and policy.

AI is like robots, but for cognitive work and services. Instead of welding, it does customer support, drafting, analytics, low‑end programming, even some chunk of “creative.”

We already see the opening credits:

- Tech firms with double‑digit earnings growth cutting tens of thousands of jobs, explicitly citing “AI efficiencies.”

- Banks, call centers, content farms running pilots that replace hundreds of roles per deployment, not tens.

We covered the structural angle in AI and job displacement: at current capability levels, a scary fraction of routine office and service work is technically automatable.

That’s not deflation yet. It’s the pressure building in the pipes.

2. Frictions are slowing the hit, for now

Citi points out the usual brakes:

- Adoption friction: integrating AI into workflows is hard; the “agent that just works” is still mostly slideware.

- Regulation and liability: sectors like healthcare, finance, and government can’t just YOLO an LLM into production.

- Energy and capex constraints: inference at scale is expensive; data centers, grid capacity, and chips are real bottlenecks.

These frictions buy time. They don’t change the sign of the effect.

From a builder perspective: every quarter the tooling gets better, the “last mile” integrations get simpler, and the ROI story for replacing people with agents gets cleaner. Once you cross a usability and trust threshold, the lag disappears frighteningly fast.

3. Policy can easily overpower the tech, in either direction

Here’s where AI deflation really becomes a political‑economy question.

A world of:

- weak unions,

- shareholder‑maximizing corporate governance,

- regressive tax regimes,

- and an antitrust posture that shrugs at winner‑take‑all AI platforms,

is a world where AI gains will be aggressively concentrated by design.

Flip some of those knobs, wage floors, profit‑sharing norms, labor representation on boards, active antitrust, and the same AI curve produces very different macro outcomes: higher real wages, more leisure, moderate inflation, more stable demand.

The technology sets the size of the pie. Policy and power decide the slices.

Citi’s scenario becomes plausible if we do nothing and let existing power structures amplify AI’s centralizing tendencies.

What to Do Next: Policy Levers, Market Signals, and Practical Steps

If you accept that AI deflation is mostly a distributional failure, not a productivity curse, the question shifts from “are we doomed?” to “what dials can we turn?”

1. Policy levers that actually matter

If you were designing policy with Citi’s scenario in mind, you’d watch four families of tools:

- Income side (labor institutions)

- Higher minimum wages indexed to productivity.

- Sectoral bargaining or modernized unions in AI‑heavy industries.

- Earned income tax credits that scale with productivity, not just inflation.

- Ownership side

- Broad‑based equity in AI‑rich firms (ESOPs, worker stock grants, even sovereign wealth funds funded by AI profits).

- Windfall or excess‑profit taxes tied to measured productivity jumps, recycling proceeds into wage subsidies or public services.

- Product market side

- Aggressive antitrust on AI platforms and big‑tech “hub and spoke” pricing conspiracies.

- Data portability and open‑model requirements that prevent one or two incumbents from capturing all AI rent.

- Automatic stabilizers

- Strong, fast‑acting unemployment insurance and retraining.

- Automatic fiscal stabilizers that kick in when unemployment or wage share of GDP cross thresholds, rather than waiting on Congress.

Notice what’s not on this list: “pause AI.” A pause doesn’t fix the distributional plumbing; it just slows how fast existing inequalities get amplified.

2. Market and policy signals to watch (so you’re not surprised)

From an investor or just “trying to not get wrecked” standpoint, here are practical signals for AI-induced deflation risk:

- Labor share of income in AI‑intensive sectors

Are software, finance, and media’s labor shares falling even as sector output grows? If yes, concentration is winning. - Profit margins vs wage growth

If you see multi‑year margin expansion for AI leaders with stagnant or negative median wage growth, you’re in Citi‑land. - Rate cuts without wage growth

Central banks getting more dovish while unemployment drifts up and wages are flat is exactly the pattern Citi sketches. - Real‑price trends for digital services

If software/media prices start falling while consumption stalls and profits stay high, that’s excess capacity plus weak demand, filtered through monopoly power. - Policy direction

- Pro‑labor moves (wage floors, antitrust cases, union wins, profit‑sharing discussions) = lower deflation risk.

- Tax cuts for capital, weak antitrust, and “AI will self‑regulate” speeches = higher deflation risk.

3. Individual and firm‑level moves

You’re not the Fed. But you’re not powerless.

For individuals:

- Move toward “AI‑complement” roles, not “AI‑substitute” ones. Work that is:

- tied to physical presence (skilled trades, healthcare),

- high‑context and relational (management, complex sales),

- or that designs and governs AI systems themselves.

- Push for upside mechanisms where you work: equity, profit‑sharing, bonus pools explicitly linked to AI‑driven productivity.

For builders and managers:

- Design AI projects around augmentation, not pure headcount cuts.

If every AI initiative’s business case is “we fire 30%,” you’re actively building Citi’s world. - Bake in gain‑sharing: if AI cuts a team’s toil by 40%, part of that shows up as higher comp or shorter hours, not just margin.

This isn’t charity. It’s self‑preservation. Firms that treat AI as a pure worker‑replacement machine are sawing off the demand branch they sit on.

Key Takeaways

- AI deflation is not about technology being “too productive”; it’s about productivity gains being captured by a narrow elite while mass incomes stagnate.

- Citi’s warning is basically a macro version of “AI value capture”: concentrated winners, weakened labor, and central banks stuck fighting disinflation with low rates.

- The mechanisms are familiar from past automation (robots, offshoring), but AI can hit a much wider range of jobs much faster.

- Policy choices on wages, ownership, antitrust, and automatic stabilizers will decide whether AI yields abundance with demand, or a deflationary grind.

- Individuals and firms can reduce risk by treating AI as a complement (and sharing gains), not a blunt instrument for headcount cuts.

Further Reading

- Global Growth: More Resilient Than Ever, Citi Research, Citi’s own summary of the research note that raises AI, unemployment, and deflation as a macro risk scenario.

- Citi warns of deflation if AI sparks high unemployment and only benefits a small elite, Business Insider, Jennifer Sor’s coverage with the key Citi quotes on high unemployment and concentrated AI winners.

- Citi says AI disruption risk is real, timing ‘very unclear’, Investing.com, Adds detail on the strategists’ note and Citi’s caveat that timing of large disruptions is highly uncertain.

- Robots and Jobs: Evidence from US Labor Markets, Acemoglu & Restrepo, Classic empirical paper on how automation affects employment and wages, a template for thinking about AI’s labor impact.

- The Myth of AI Wrappers and Where Value Hides, NovaKnown’s take on how AI productivity gains get captured, and why platforms tend to soak up most of the value.

- Can AI Already Replace 11.7% of the U.S. Workforce?, Our analysis of which jobs are most exposed to near‑term AI displacement.

In other words: the scary part of Citi’s AI deflation note isn’t that the robots get too good. It’s that we might be lazy about power and policy while they do.